Over the last few years, credit card expenditure has been on the increase in credit card spending among households which has attracted the attention of the economists and even common consumers. Cards are becoming the standard form of payment moving away with groceries, traveling, online subscriptions as well as emergency costs. This growth is not just a mere consumer phenomenon, as the landscape of the industry was influenced by increased inflation, the digital convenience, and changing lifestyles. It represents the general economic and psychological tendencies.

Inflation Pressure

Increasing the prices has highly affected the spending habits. Food, fuel and houses are now expensive, as compared to a few years back. In case the wages are not increased in the same ratio, a significant percentage of families resort to the credit cards in order to fill the gap. Borrowing is a short term coping mechanism of sustaining the standards of daily living.

Digital Payments

Credit card has been more convenient than ever before due to online shopping and contactless payment. Using mobile wallets and one click check outs, the payments become less physical and quicker. The resistance that used to occur when passing over the cash has been eliminated and more people tend to buy more and occasionally buy impulsively.

Easy Access

Pre approved offers and instant digital applications have helped financial institutions to increase credit access. Walmart big names such as American Express and Chase advertise reward based cards which are attractive to the large masses of consumerism. Good sign up bonuses and cashback reward should be used as an incentive to increase usage.

Rewards Culture

Reward programs have a powerful psychological implication to the spending behavior. The illusion of making money in the process of spending is formed by the points, miles, and cashback offers. Card programs intimately attached to airline companies or the brands of hotels, even more encourage cardholders to channel their daily spending through a card, and not through a debit card.

Lifestyle Expectations

Consumption habits are affected by social media and new tendencies in the modern lifestyle. Activities like traveling, eating and out, or high-quality subscriptions are seen as a necessity but not a luxury. A credit card offers the convenience to have any experience of such later (although it may pay later).

Emergency Buffer

One will find themselves using their card unexpectedly due to sudden medical expenses, auto repairs, or house repairs. Most households use revolving credit as a last resort in case of emergencies and this has happened due to the lack of emergency savings. Although this is convenient, there is the problem of the high interest rates that may be cumbersome to repay over the years.

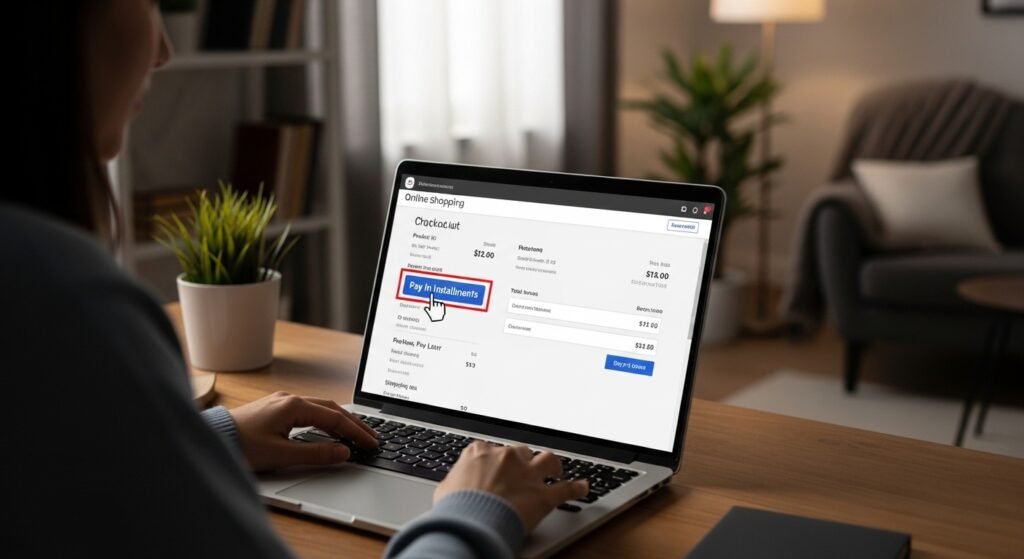

BNPL Impact

BNPL services have transformed the consumer expectations in terms of flexible payments. As such services continue to be combined with conventional credit mechanisms, the way people spend is adopting the mode of Installment based purchasing. The trend has normalized the consumption of borrowed money to live via consumption, not through making big purchases that are once in a lifetime.

Interest Rate Dynamics

The credit cards have become very popular even with the increased interest rates that are experienced due to low minimum payments structures which give individuals less financial strain. Borrowers can emphasize on low cost short term rather than high cost long term and this leads to long term high balances on many accounts.

Economic Uncertainty

The economic uncertainty periods tend to create mixed reactions on the consumer response. Other individuals are spending less, and others are taking up more credit to keep things afloat. Uncertainty about the future and the nature of the income may result in the level of short term borrowing in order to settle the routine liabilities.

Behavioral Factors

There is a potent role of psychology in the use of credit cards. Swiping or tapping is less painful compared to cash which makes it less conscious the money is leaving your account. This behavioral impact in the long run may be a slow growth in expenditure as compared to initially planned budgets.