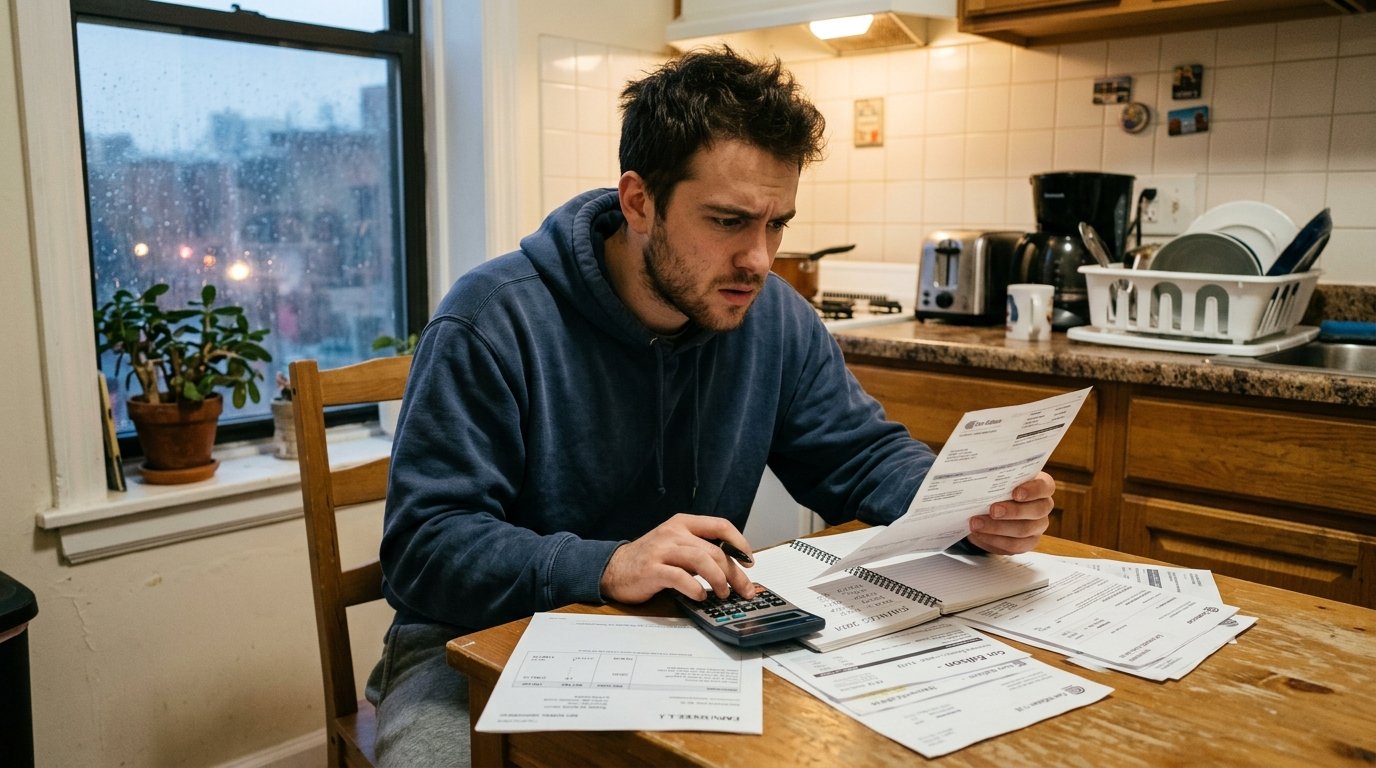

Walk into a bank today with the same application you brought two years ago and there is a real chance you walk out empty handed. Nothing changed on your end. The rules changed on theirs. Quietly, without much warning, lending got tighter across almost every category and regular people are bearing the cost of that shift right now.

Getting Approved Is Harder

Lenders who were relaxed about certain numbers are now digging into everything. Same income, same job, same history – different answer than you would have gotten before.

Credit Score Goalposts Shifted

Numbers that used to clear the bar comfortably are sitting in gray zones now. Nobody sent an email about it. People just started finding out the hard way when applications came back denied.

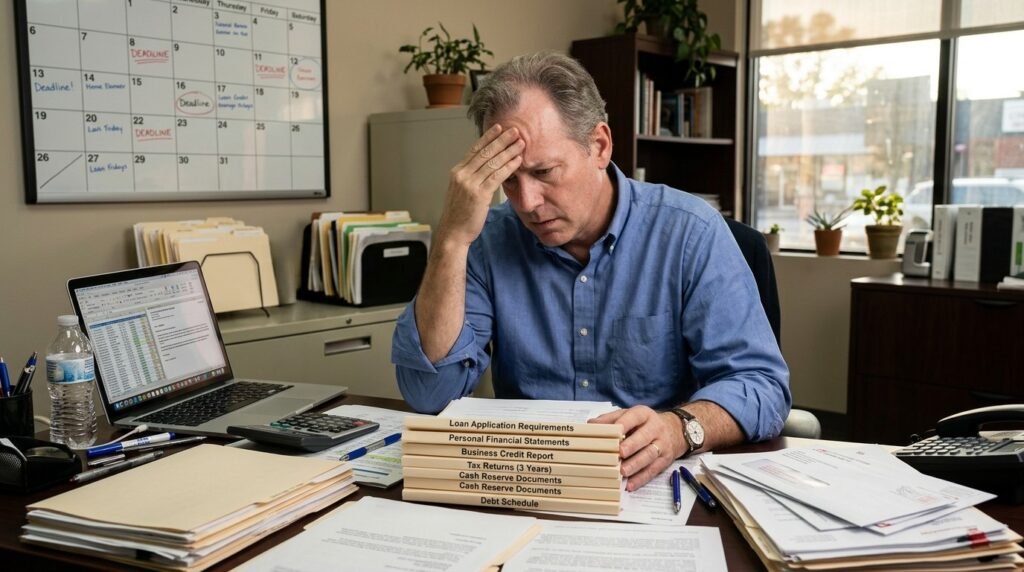

Small Business Owners Took a Hit

Used to be a decent revenue history got you through. Now lenders want personal credit, business credit, cash reserves, and documentation for all of it. Owners who never struggled before are struggling now.

Card Limits Dropped Without Warning

No missed payments. No red flags. Just an app notification one morning showing a lower limit and a vague letter that arrived three days later explaining essentially nothing.

Buying a Car Got Expensive Fast

Rates on approved loans are sitting at levels that turn a reasonable car into an uncomfortable monthly commitment. Dealers who used to find financing for almost anyone are sending people home more than they used to.

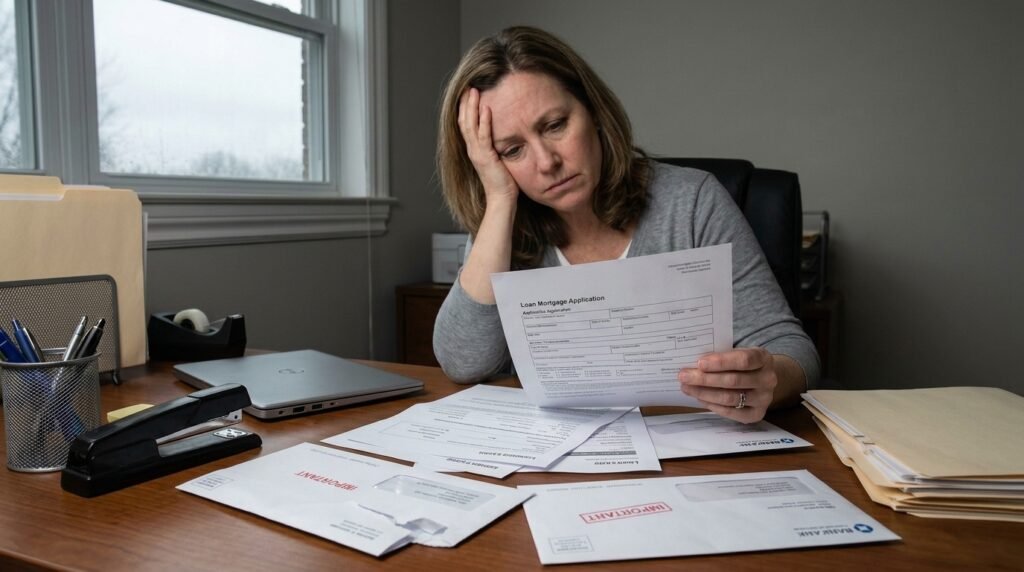

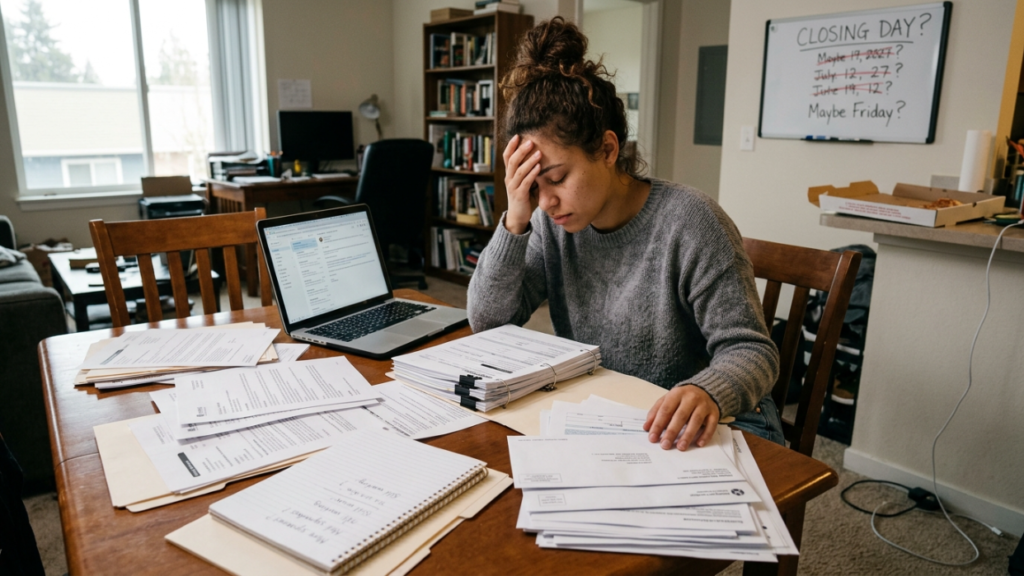

Mortgage Process Slowed Down

More documents, more conditions, more back and forth after you thought things were settled. First timers are exhausted before they even get close to closing and people who have done it before say it never used to feel like this.

Renting Got Harder Too

Landlords tightened their screening around the same time banks did. Credit checks that were formalities became actual filters. Income requirements went up. The rental market started feeling like a loan application.

Buy Now Pay Later Is Costing People

Those easy payment splits that felt harmless are appearing on credit reports at more lenders now. A few open balances looks like a risk flag even when every single payment has been on time.

First-Time Borrowers Got Blindsided

Never experienced a tighter cycle so they had nothing to compare it against. The process felt broken to them. It was not broken. It just changed overnight and nobody explained that clearly to anyone.

Rising Delinquencies Changed Everything

Quietly, across enough borrowers, missed payments started ticking up. Risk departments noticed, adjusted their models, and the whole system recalibrated. Regular applicants are now living inside that recalibration without fully understanding why.

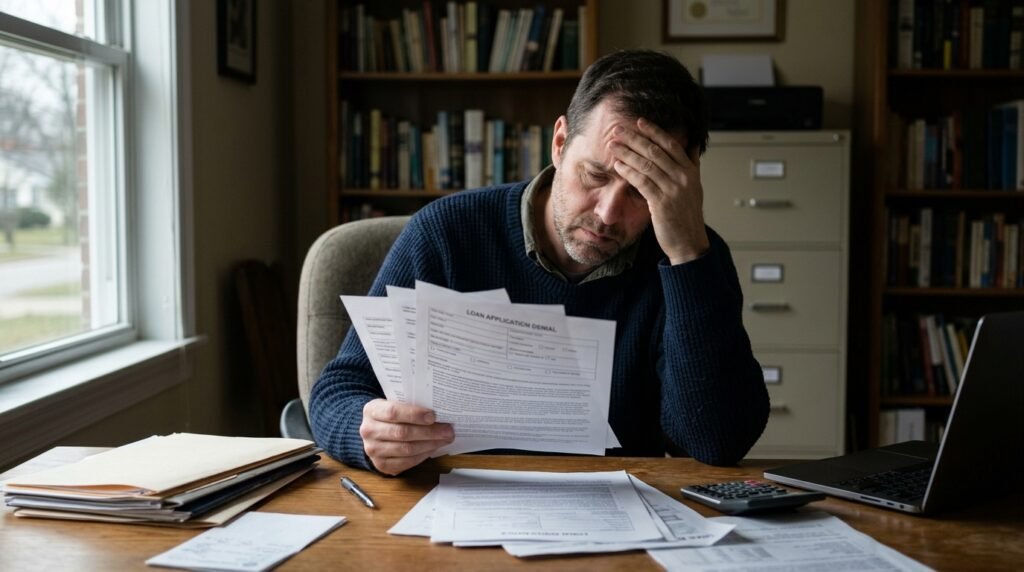

Lenders Not Explaining Themselves

Denial letters say very little. Conditions appear late. Timelines shift without communication. Half the frustration borrowers feel is not even about the rejection. It is about being kept completely in the dark through the whole process.

Younger Borrowers Feeling It Most

Less history, less savings, less traditional employment in some cases. Every box lenders are now scrutinizing harder is a box younger applicants were already weaker in before the rules even tightened.

What Still Actually Works

Get balances down before applying for anything significant. Avoid opening new accounts in the months before a big application. Have every document ready before anyone asks. Right now the difference between a prepared applicant and an unprepared one is bigger than it has been in a very long time.