The historical period before people used digital banking methods and credit cards created an unusual experience that changed how people exchanged value. Throughout history, people used various items as money because communities decided which things held value. The historical review of these systems demonstrates the essential requirement of trust together with imagination to operate the worldwide economic system.

Giant Stones as Bank Accounts

On the island of Yap, people used “Rai stones” , massive limestone disks as currency. The stones had such extreme weight that people could not move them from their original locations therefore when people spent one the community accepted that the stone had transferred ownership to the new person but the stone remained untouched at its position.

Salt as a Monthly Salary

In Ancient Rome, soldiers were sometimes paid in salt because it was essential for preserving food, the word “salary” originates from this particular term and the soldier lost his ability to purchase dinner because he failed to perform his duties according to his expected level of performance.

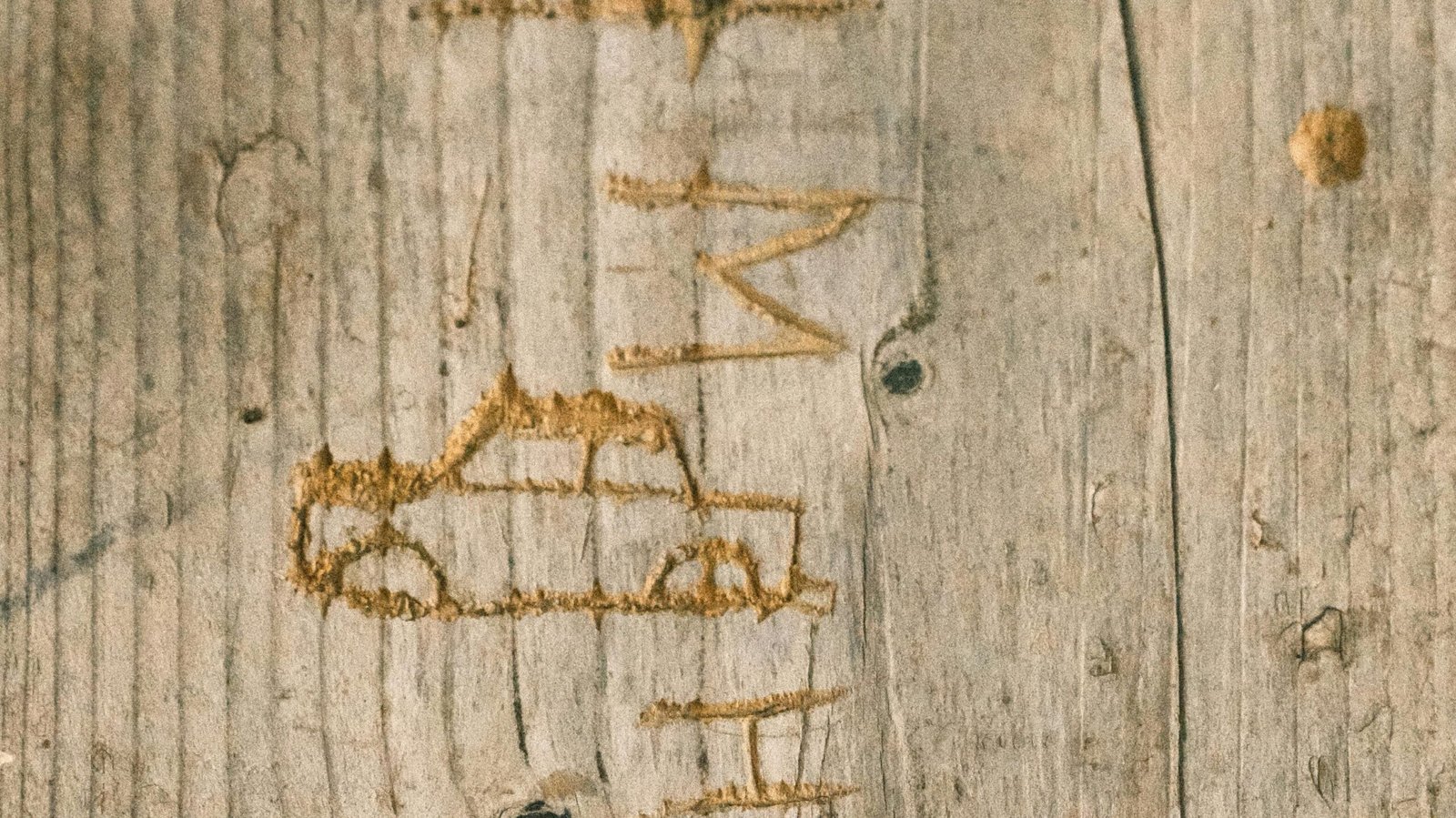

The “Broken Stick” Receipts

For centuries, the British Treasury used “Tally Sticks” to track debt. A wooden stick was notched to show the amount owed and then split down the middle. Both parties kept one half, and they only “validated” the payment when the two pieces fit back together perfectly.

Tulip Mania in the Netherlands

In the 1630s, a tulip bulb from a rare variety could sell for more than an expensive house in Amsterdam and the market crashed when people believed flower prices would keep rising therefore they spent their entire savings on flowers which resulted in them ending up with nothing except garden plants.

Cowrie Shells for Global Trade

Small seashells served as the world’s most common form of currency for thousands of years. The durable shells from Africa and Asia served as a global “dollar” which people could carry easily while merchants needed to copy every single item that became available before paper money came into existence.

The First Paper Money “Experiment”

In 10th-century China, merchants grew tired of carrying heavy iron coins. Merchants stopped transporting their coins and instead they used “deposit notes” to carry their funds after leaving their coins with trusted officials. This was the beginning of paper money which was built on the trust that iron coins still existed as physical currency.

Livestock as a Walking Wallet

Ancient societies considered cattle ownership to be the main way of measuring a person’s material wealth. To buy land or pay a dowry, people needed to bring a herd of cows to the seller instead of using coins. The currency had the ability to create food which maintained its value.

Cocoa Beans as “Small Change”

The Aztecs used cocoa beans for everyday purchases and a small snack might cost a few beans, while a high-quality cloak could cost 100. The currency allowed people to turn their savings into drinkable form provided they consumed the actual savings.

Peppercorn Rents

During the Middle Ages, black pepper was so valuable it was called “Black Gold” and landlords would often accept a single pound of peppercorns as a year’s rent. The term “peppercorn rent” describes a payment that exists either as a minimal amount or a representation of something valuable.